Cell Name | Field Definition |

1 | RecordType | The type of the Record which shall always contain the value SRD1. |

2 | RecordId | The Identifier of this single record revenue retails record which shall be specific to the RevenueDetails. |

3 | CurrencyOf Accounting | The currency in which the values in the revenue Cells are accounted (represented by an ISO 4217 CurrencyCode). |

4 | NetRevenueIn CurrencyOf Accounting | The revenue generated from the licensing of sound recordings, music videos and/or audio-visual resources containing music in the CurrencyOfAccounting. This amount is the aggregate of the net revenue amounts that appear in the relevant revenue Cells. |

5 | SummaryRecordId | The identifier of the SRS1 Record to which this Record provides details to. This Cell is mandatory if a RevenueSummarymessage has been sent. |

6 | StatementType | The description of the type of the revenue details data being provided in this RevenueDetails message. If a RevenueSummary message has been sent, this Cell will be the same as the SummaryType of the SRS1 Record with the RecordId given by the SummaryRecordIdCell. |

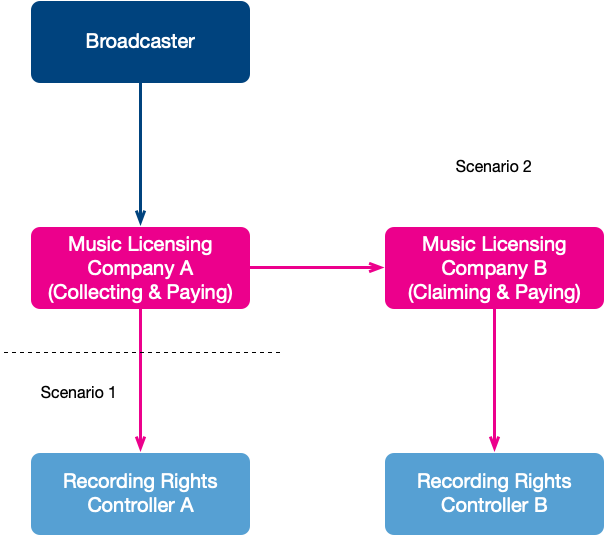

7 | CollectingMlcName | The name of the collecting music licensing company (for music licensing company to music licensing company to payee use cases). |

8 | PayingMlcName | The name of the paying music licensing company. |

9 | ClaimingMlcName | The name of the claiming music licensing company. |

10 | ClaimingMlc AllocatedPartyId | A proprietary identifier allocated by the claiming music licensing company to the party to whom the relevant revenue has been allocated. This is preceded by a namespace identifier in the syntax ns::id. |

11 | PayingMlc AllocatedPartyId | A proprietary identifier allocated by the paying music licensing company to the party to whom the relevant revenue has been allocated. This is preceded by a namespace identifier in the syntax ns::id. |

12 | AllocatedPartyIPN | The International Performer Number allocated to the party to whom the relevant revenue has been allocated. An IPN is an 8-digit integer. |

13 | AllocatedPartyISNI | The International Standard Name Identifier allocated to the party (whether a legal entity or natural person) to whom the relevant revenue has been allocated. |

14 | AllocatedParty FullName | The complete name of the party, in its normal form of presentation to whom the relevant revenue has been allocated. This can be a record company if the value in the SummaryType Cell is RightsController, or a party that has contributed to the resource if the value in the SummaryType is Contributor. |

15 | ResourceType | The type of the resource (sound recordings, music videos and/or audio-visual resource containing music) to which the revenue which is the subject of this Record is allocated. If this Record needs to communicate other types of revenue not directly attributable to a resource the ResourceType should be None. |

16 | AudioVisualType | The type of audio-visual resource to which is determined by the nature of the content of the audio-visual resource. This Cell is mandatory if the ResourceType is Video. |

17 | RevenueAllocationType | The functional nature of the audio-visual resource to which revenue has been allocated. This Cell is mandatory if ResourceType is Video. |

18 | ISRC | The ISRC (International Standard Recording Code as defined in ISO 3901) for the sound recording or music video. An ISRC comprises four parts: two characters, followed by three alphanumeric characters, then two digits and five digits. |

19 | ISAN | An identifier of the audio-visual resource allocated in accordance with the International Standard Audio-visual Number as defined in ISO 15706. |

20 | EIDR | An identifier of the audio-visual resource allocated in accordance with the Entertainment Identifier Registry. |

21 | Proprietary ResourceId | A proprietary identifier allocated by the music licensing company that is the sender of the message to the resource to which the relevant revenue has been allocated. This is preceded by a namespace identifier in the syntax ns::id. Provision of a ProprietaryResourceId is mandatory if there is no ISRC provided. |

22 | ResourceTitle | The title of the resource if provided. This Cell is mandatory if ResourceType is not None. |

23 | ResourceSubTitle | A descriptor which is supplementary to, but not contained within, a Title. |

24 | SeriesTitle | The title of the series of which the audio-visual resource is a part. |

25 | SeasonNumber | The number of the season of the series of which the audio-visual resource is a part. |

26 | EpisodeNumber | The number indicating the order of the episodes within a season (if available) or series. |

27 | Genre | The genre of the work. |

28 | Resource DisplayArtistName | The name of the display artist of the resource to which the relevant revenue has been allocated as notified to the music licensing company that is the sender of the message by the relevant rights controller. This Cell is mandatory if ResourceType is SoundRecording or MusicVideo. |

29 | HasMadeFeatured Contribution | A flag indicating whether the party to whom the relevant revenue has been allocated is considered to have made a prominently featured contribution (=true) or not (=false). |

30 | HasMadeContracted Contribution | A flag indicating whether the party to whom the relevant revenue has been allocated made the contribution to the resource under an exclusive contract with the initial producer (=true) or not (=false). |

31 | AudioVisual ContributorName | The name of a contributor to the audio-visual resource. This information is purely for the purpose of helping to identify the resource to which revenue has been allocated. This Cell does not specify the party to whom revenue has been allocated for a contribution to the resource. The order of the individual data elements in AudioVisualContributorNameand AudioVisualContributorRole Cellsshall be the same so that the recipient is able to relate them correctly. This Cell is mandatory if a AudioVisualContributorRole is provided. |

32 | AudioVisual ContributorRole | The description of the roles(s) of the contributor in the AudioVisualContributorName Cell. The number and order of the individual data elements in the AudioVisualContributorName and AudioVisualContributorRole Cells shall be the same so that the recipient is able to relate them correctly. A value in this Cell is mandatory if a AudioVisualContributorName is provided. |

33 | AllocatedPartyC ontributionRole | The description of the role(s) of the party to whom revenue has been allocated for a contribution to the resource. If multiple roles are to be communicated, multiple SRD1 records must be provided. |

34 | AllocationShare Percentage | The percentage of gross revenue allocated to the AllocatedPartyFullName in relation to the resource. If the value in the SummaryType Cell is RightsController, the provision of a value in this Cell is mandatory and relates to a record company’s ownership share in that resource. If the value in the SummaryType Cell is Contributor, the provision of a value in this Cell is optional and the percentage of gross revenue is allocated to the AllocatedPartyFullName in relation to the AllocatedPartyContributionRole if provided. A quarter share is represented by “25” (and not 0.25). |

35 | ICPN | The ICPN used as proxy for identification of the release. An ICPN comprises 12 or 13 digits, depending on whether it is an EAN (13) or a UPC (12). 14 character ICPNs are also permitted. |

36 | ReleaseCatalog Number | The catalogue number of the release assigned by the issuing record company. |

37 | AudioVisual ProductionDate | The date when the audio-visual resource was produced, in the ISO 8601 format: YYYY[-MM[-DD]]. |

38 | AudioVisual CreationDate | The date when the audio-visual resource was created, in the ISO 8601 format: YYYY[-MM[-DD]]. |

39 | TerritoryOf RevenueGeneration | The territory in which the revenue was generated. This Cell is mandatory unless ResourceType is None. |

40 | UseType | A type of usage that a licensee of the relevant music licensing company has made of the resource and for which the revenue has been generated. If multiple UseTypes are to be communicated, multiple SRD1 records must be provided. |

41 | LicenseeName | The name of the licensee of the relevant music licensing company whose output has generated the revenue. |

42 | LicenseeId | The PartyId of the licensee the relevant music licensing company. |

43 | UsageSourceName | The name of the source of usage reporting that has been used to allocate revenue to the resource. |

44 | UsageSourceId | The PartyId of the UsageSource. |

45 | AllocationGuidance | A description of the nature of changes that may have occurred to the resource to which the revenue has been allocated. For example, a resource may have been a previously unidentified recording, or a resource was in conflict and this is solved, or the rights controller of a resource has changed). |

46 | UsageStartDate | The date of the start of the usage period to which the revenue which is the subject of the Record relates, in ISO 8601 format. This is a string with the syntax YYYY[-MM[-DD]]. This Cell is mandatory if ResourceType is not None. |

47 | UsageEndDate | The date of the end of the usage period to which the revenue which is the subject of the Record relates, in ISO 8601 format. This is a string with the syntax YYYY[-MM[-DD]]. This Cell is mandatory if ResourceType is not None. |

48 | Recipient RevenueType | A description of the type of revenue that indicates on behalf of whom the revenue was collected. This Cell is mandatory if ResourceType is not None. |

49 | RevenueSourceType | A type of revenue earned by the resource, according to the way the revenue is generated. This Cell is mandatory if ResourceType is not None. |

50 | RevenuePoolName | A description of the type of licensee, whether a single licensee or multiple licensees, which forms the source of the revenue being allocated. |

51 | BasisFor RevenueAllocation | A description of the nature of the data used to determine the distribution of revenue, for example a usage log or a full census. |

52 | UnitTypeFor RevenueAllocation | The basis applied to each unit of usage as part of the process of revenue allocation which is the subject of this Record. It is possible to have mixed types within a RevenueReportmessage. |

53 | UnitRate | The rate applied to each unit of usage in the CurrencyOfAccounting. |

54 | Usages | The number of units of usage of the resource. |

55 | Reallocation FromNonQualifying Performance | Revenue allocated to a performance which does not qualify for equitable remuneration and is re-allocated to the rights controller. |

56 | CollectingMlc GrossAmount | The gross amount of revenue collected by the collecting music licensing company's in the CurrencyOfAccounting. |

57 | PayingMlc GrossAmount | The gross amount of revenue being paid by the paying music licensing company's gross amount in the CurrencyOfAccounting. |

58 | CollectingMlc Commission | The collecting music licensing company's amount of commission or administrative fee(s) in the CurrencyOfAccounting. This amount is deducted from the CollectingMlcGrossAmount and is therefore a negative number. An adjustment to commission or administrative fee(s), which will be added to the CollectingMlcGrossAmount, can be expressed by using a positive number. |

59 | PayingMlcCommission | The paying music licensing company's amount of commission or administrative(s) fee in the CurrencyOfAccounting. This amount is deducted from the PayingMlcGrossAmountand is therefore a negative number. An adjustment to commission or administrative fee(s), which will be added to the PayingMlcGrossAmount, can be expressed by using a positive number. |

60 | CollectingMlcSocialCulturalDeduction | The collecting music licensing company's social and cultural deduction amount in the CurrencyOfAccounting. This amount is deducted from the CollectingMlcGrossAmount and is therefore a negative number. An adjustment to social and cultural deduction(s) to the CollectingMlcGrossAmount can be expressed by using a positive number. |

61 | PayingMlcSocialCulturalDeduction | The paying music licensing company's social and cultural deduction amount in the CurrencyOfAccounting. This amount is deducted from the PayingMlcGrossAmountand is therefore a negative number. An adjustment to the social and cultural deduction(s) to the PayingMlcGrossAmountcan be expressed by using a positive number. |

62 | CollectingMlc AdministrationCost Deduction | The collecting music licensing company's deduction for administration costs in the CurrencyOfAccounting. This amount is deducted from the CollectingMlcGrossAmount and is therefore a negative number. An adjustment of the administrative costs to theCollectingMlcGrossAmount can be expressed by using a positive number. |

63 | PayingMlc AdministrationCost Deduction | The paying music licensing company's deduction for administration costs in the CurrencyOfAccounting. This amount is deducted from the PayingMlcGrossAmountand is therefore a negative number. An adjustment to the administrative costs to thePayingMlcGrossAmount can be expressed by using a positive number. |

64 | CollectingMlcOther Deduction1 | The collecting music licensing company's other deduction amount in the CurrencyOfAccounting. This amount is deducted from the CollectingMlcGrossAmount and is therefore negative numbers. An adjustment of the other deduction to the CollectingMlcGrossAmount can be expressed by using a positive number. |

65 | CollectingMlcOther DeductionType1 | The type of deduction specified in the CollectingMlcOtherDeduction1 Cell. A value in this Cell is mandatory if there is a value in the CollectingMlcOtherDeduction1 Cell. |

66 | PayingMlcOther Deduction1 | The paying music licensing company's other deduction amount in the CurrencyOfAccounting. This amount is deducted from the PayingMlcGrossAmountand is therefore negative numbers. An adjustment of the other deduction to the PayingMlcGrossAmount can be expressed by using a positive number. |

67 | PayingMlcOther DeductionType1 | The type of deduction specified in the PayingMlcOtherDeduction1 Cell. A value in this Cell is mandatory if there is a value in the PayingMlcOtherDeduction1Cell. |

68 | CollectingMlcOther Deduction2 | The collecting music licensing company's other deduction amount in the CurrencyOfAccounting. This amount is deducted from the CollectingMlcGrossAmount and is therefore negative numbers. An adjustment of the other deduction to the CollectingMlcGrossAmount can be expressed by using a positive number. |

69 | CollectingMlcOther DeductionType2 | The type of deduction specified in the CollectingMlcOtherDeduction2 Cell. A value in this Cell is mandatory if there is a value in the CollectingMlcOtherDeduction2 Cell. |

70 | PayingMlcOther Deduction2 | The paying music licensing company's other deduction amount in the CurrencyOfAccounting. This amount is deducted from the PayingMlcGrossAmountand is therefore negative numbers. An adjustment of the other deduction to the PayingMlcGrossAmount can be expressed by using a positive number. |

71 | PayingMlcOther DeductionType2 | The type of deduction specified in the PayingMlcOtherDeduction2 Cell. A value in this Cell is mandatory if there is a value in the PayingMlcOtherDeduction2Cell. |

72 | CollectingMlcOther Deduction3 | The collecting music licensing company's other deduction amount in the CurrencyOfAccounting. This amount is deducted from the CollectingMlcGrossAmount and is therefore negative numbers. An adjustment of the other deduction to the CollectingMlcGrossAmount can be expressed by using a positive number. |

73 | CollectingMlcOther DeductionType3 | The type of deduction specified in the CollectingMlcOtherDeduction3 Cell. A value in this Cell is mandatory if there is a value in the CollectingMlcOtherDeduction3 Cell. |

74 | PayingMlcOther Deduction3 | The paying music licensing company's other deduction amount in the CurrencyOfAccounting. This amount is deducted from the PayingMlcGrossAmountand is therefore negative numbers. An adjustment of the other deduction to the PayingMlcGross Amount can be expressed by using a positive number. |

75 | PayingMlcOther DeductionType3 | The type of deduction specified in the PayingMlcOtherDeduction3 Cell. A value in this Cell is mandatory if there is a value in the PayingMlcOtherDeduction3Cell. |

76 | CollectingMlcOther Deduction4 | The collecting music licensing company's other deduction amount in the CurrencyOfAccounting. This amount is deducted from the CollectingMlcGrossAmount and is therefore negative numbers. An adjustment of the other deduction to the CollectingMlcGrossAmount can be expressed by using a positive number. |

77 | CollectingMlcOther DeductionType4 | The type of deduction specified in the CollectingMlcOtherDeduction4 Cell. A value in this Cell is mandatory if there is a value in the CollectingMlcOtherDeduction4 Cell. |

78 | PayingMlcOther Deduction4 | The paying music licensing company's other deduction amount in the CurrencyOfAccounting. This amount is deducted from the PayingMlcGrossAmountand is therefore negative numbers. An adjustment of the other deduction to the PayingMlcGrossAmount can be expressed by using a positive number. |

79 | PayingMlcOther DeductionType4 | The type of deduction specified in the PayingMlcOtherDeduction4 Cell. A value in this Cell is mandatory if there is a value in the PayingMlcOtherDeduction4Cell. |

80 | CollectingMlc OtherDeduction5 | The collecting music licensing company's other deduction amount in the CurrencyOfAccounting. This amount is deducted from the CollectingMlcGrossAmount and is therefore negative numbers. An adjustment of the other deduction to the CollectingMlcGrossAmount can be expressed by using a positive number. |

81 | CollectingMlc OtherDeductionType5 | The type of deduction specified in the CollectingMlcOtherDeduction5 Cell. A value in this Cell is mandatory if there is a value in the CollectingMlcOtherDeduction5 Cell. |

82 | PayingMlcOther Deduction5 | The paying music licensing company's other deduction amount in the CurrencyOfAccounting. This amount is deducted from the PayingMlcGrossAmountand is therefore negative numbers. An adjustment of the other deduction to the PayingMlcGrossAmount can be expressed by using a positive number. |

83 | PayingMlcOther DeductionType5 | The type of deduction specified in the PayingMlcOtherDeduction5 Cell. A value in this Cell is mandatory if there is a value in the PayingMlcOtherDeduction5Cell. |

84 | CollectingMlc Interest | The collecting music licensing company's interest amount in the CurrencyOfAccounting. This amount is added to the CollectingMlcGrossAmountand is therefore a positive number. An adjustment of the interest to the CollectingMlcGrossAmount can be expressed by using a negative number. This Cell is mandatory if a value is provided in the CollectingMlcInterestWithholdingTaxCell. |

85 | PayingMlcInterest | The paying music licensing company's interest amount in the CurrencyOfAccounting. This amount is added to the PayingMlcGrossAmount and is therefore a positive number. An adjustment of the interest to the PayingMlcGrossAmount, can be expressed by using a negative number. This Cell is mandatory if a value is provided in the PayingMlcInterestWithholdingTaxCell. |

86 | CollectingMlcInterestWithholdingTax | The collecting music licensing company's withholding tax amount for the deduction due to interest in the CurrencyOfAccounting. This amount is deducted from the CollectingMlcGrossAmount and is therefore a negative number. An adjustment, which will be added to the gross amount, can be expressed by using a positive number. |

87 | PayingMlcInterestWithholdingTax | The paying music licensing company's withholding tax amount for the deduction due to interest in the CurrencyOfAccounting. This amount is deducted from the gross amount and therefore a negative number. An adjustment, which will be added to the gross amount, can be expressed by using a positive number. |

88 | CollectingMlcRoyaltyWithholdingTax | The collecting music licensing company's withholding tax amount for the deduction due to royalties in the CurrencyOfAccounting. This amount is deducted from the gross amount and therefore a negative number. An adjustment, which will be added to the gross amount, can be expressed by using a positive number. |

89 | PayingMlcRoyaltyWithholdingTax | The paying music licensing company's withholding tax amount for the deduction due to royalties in the CurrencyOfAccounting. This amount is deducted from the gross amount and therefore a negative number. An adjustment, which will be added to the gross amount, can be expressed by using a positive number. |

90 | CollectingMlcOtherWithholdingTax | The collecting music licensing company’s withholding tax amount, which may be a cumulative amount that cannot be split up into more specific tax amounts or an amount of a specific type other than interest or royalty tax. This amount is given in the CurrentOfAccounting. This amount is deducted from the CollectingMlcGrossAmount and is therefore a negative number. An adjustment, which will be added to the gross amount, can be expressed by using a positive number. |

91 | PayingMlcOtherWithholdingTax | The paying music licensing company’s withholding tax amount, which may be a cumulative amount that cannot be split up into more specific tax amounts or an amount of a specific type other than interest or royalty tax. This amount is given in the CurrentOfAccounting. This amount is deducted from the PayingMlcGrossAmount and is therefore a negative number. An adjustment, which will be added to the gross amount, can be expressed by using a positive number. |

92 | CollectingMlcVAT | The VAT amount of the collecting music licensing company in the CurrencyOfAccounting. This amount is added to the CollectingMlcGrossAmount and is therefore a positive number. An adjustment, which will be subtracted from the gross amount, can be expressed by using a negative number. |

93 | PayingMlcVAT | The VAT amount of the paying music licensing company in the CurrencyOfAccounting. This amount is added to the PayingMlcGrossAmount and is therefore a positive number. An adjustment, which will be subtracted from the gross amount, can be expressed by using a negative number. |

94 | NetAmount | The final amount of revenue due following all deductions and/or additions to the relevant music licensing company’s gross amount in the CurrencyOfAccounting |